---

title: "State Of Technology 2025"

author: "Vin Patel"

url: "https://books.vinpatel.com/11/state-of-technology-2025"

---

# Executive Summary

The technology landscape of 2025 is defined by unprecedented AI investment, rapid enterprise adoption, and the emergence of autonomous AI systems that are fundamentally reshaping how businesses operate.

## AI Dominates Investment

AI captured 49% of all global venture funding in 2025, with total investment reaching $202.3 billion—a 75% increase year-over-year. This concentration of capital represents the largest technology investment supercycle since the dot-com era, but with fundamentally stronger underlying economics.

Foundation model companies alone raised $80 billion, with OpenAI ($500B valuation) and Anthropic ($183B) representing nearly 10% of all unicorn value globally.

## Enterprise AI Accelerates

78% of organizations now deploy AI in production, up from 55% in 2023. This isn't experimental adoption—it's operational transformation.

Enterprise GenAI spending surged to $37 billion, a 3.2x increase from 2024. More significantly, the "buy vs. build" equation has flipped: 76% of AI use cases are now purchased rather than built internally, reflecting the maturity of commercial AI products.

## Agentic AI Emerges

Autonomous AI agents represent the next frontier. 79% of organizations report agentic AI adoption, with an average ROI of 171% and task time reductions of 86%.

By 2028, Gartner projects 15% of day-to-day work decisions will be made autonomously by agentic AI—up from 0% in 2024. The agent workforce revolution is no longer theoretical.

---

*The pages that follow provide detailed analysis, data, and strategic guidance for navigating this transformative moment in technology history.*

# The AI Investment Supercycle

*Unprecedented capital concentration reshapes the technology landscape*

## Record-Breaking Investment

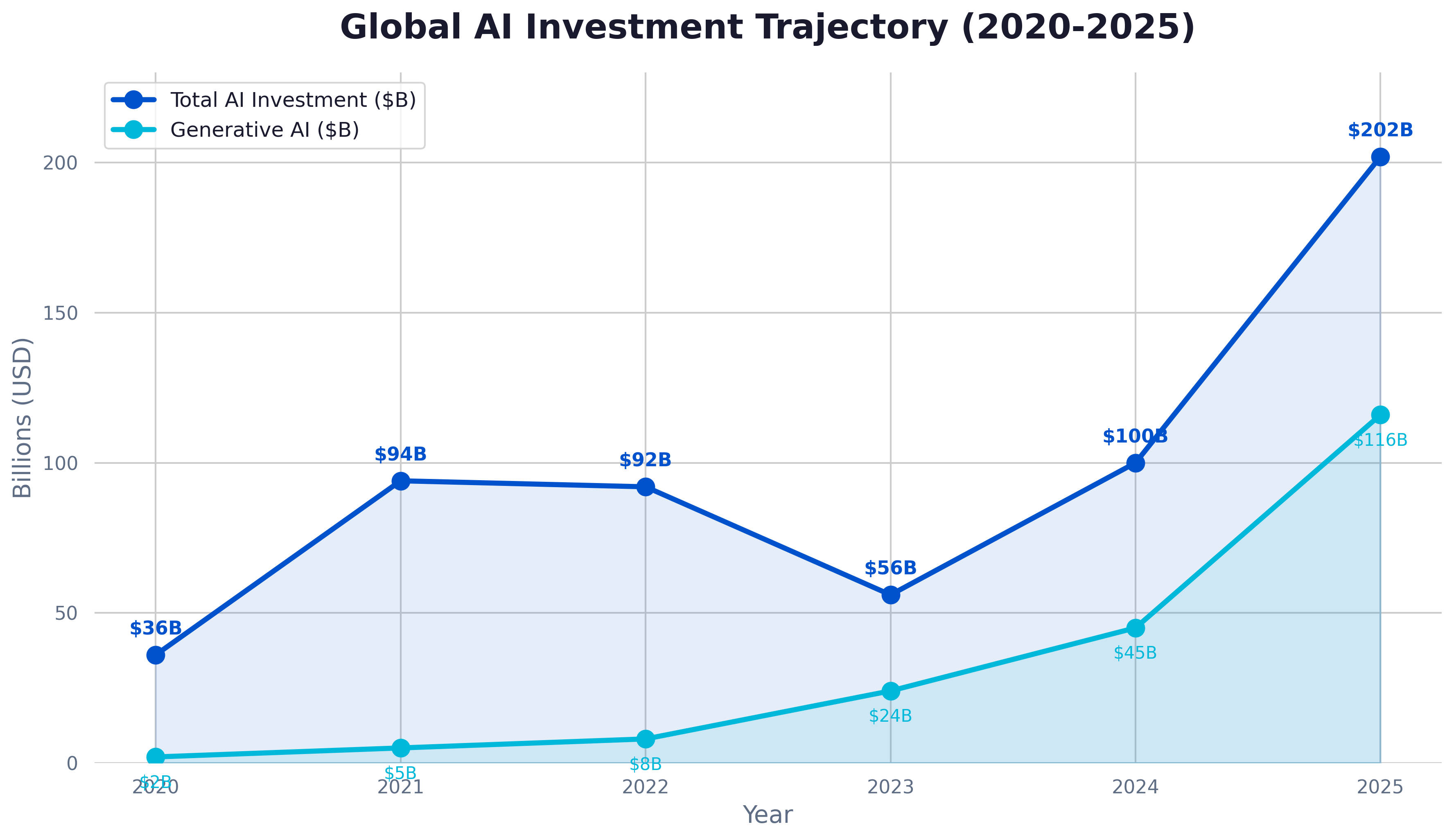

2025 marks an inflection point in technology investment history. Global AI investment reached $202.3 billion—more than double the $100 billion invested in 2024 and representing a 75% year-over-year increase.

To put this in perspective: AI now captures 49% of all global venture funding. Nearly half of every venture dollar flows into artificial intelligence.

## The Trajectory (2020-2025)

| Year | Total AI Investment | Generative AI |

|------|--------------------:|--------------:|

| 2020 | $36B | $2B |

| 2021 | $94B | $5B |

| 2022 | $92B | $8B |

| 2023 | $56B | $24B |

| 2024 | $100B | $45B |

| 2025 | $202B | $116B |

The 2023 dip—often called the "AI winter scare"—proved to be a brief pause before explosive growth. Generative AI investment alone grew from $24B to $116B in just two years.

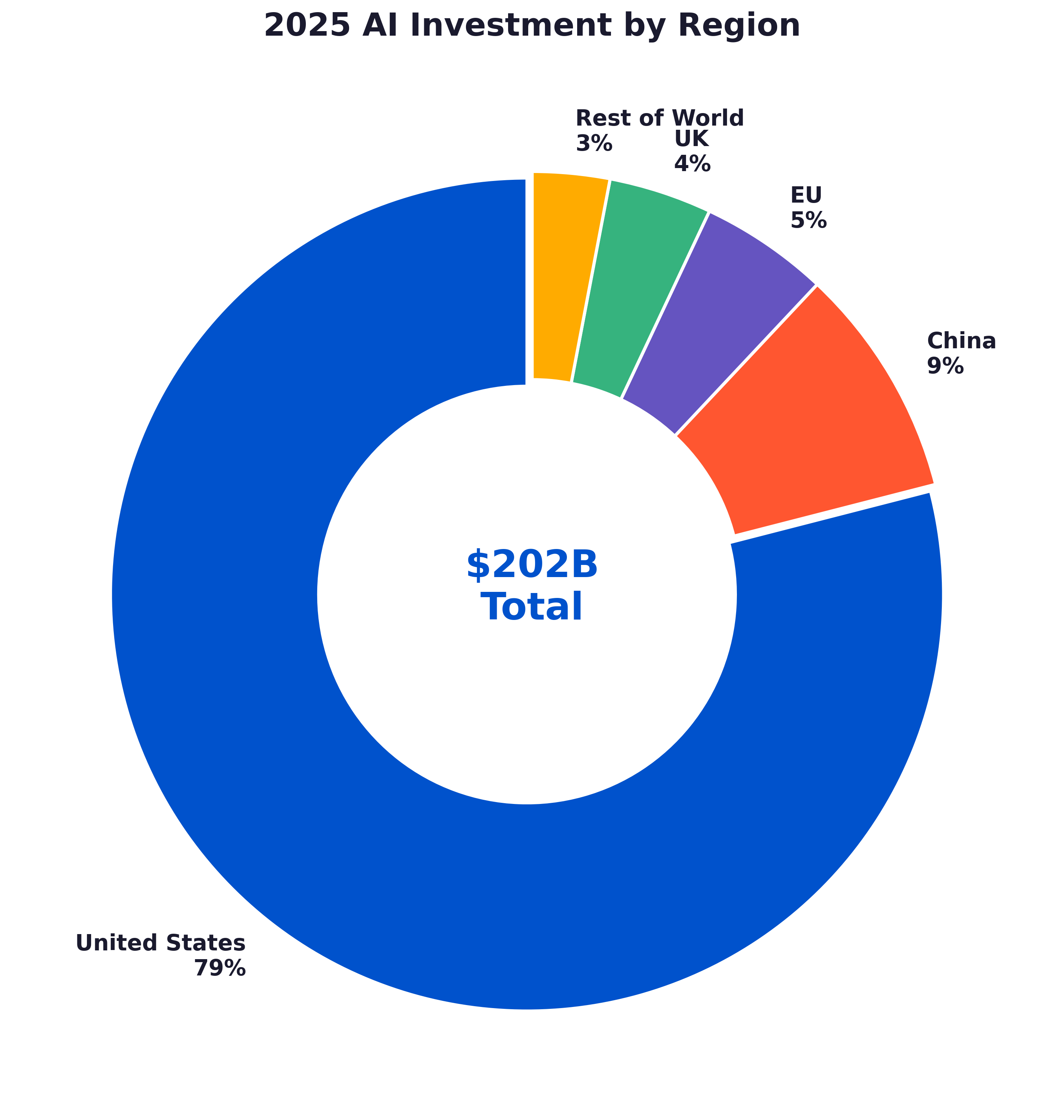

## Regional Dominance

The United States has established overwhelming dominance in AI investment:

- **United States**: 79% ($159B)

- **China**: 9% ($18B)

- **European Union**: 5% ($10B)

- **United Kingdom**: 4% ($8B)

- **Rest of World**: 3% ($6B)

US-based companies captured nearly 8 out of every 10 AI investment dollars globally.

## The Foundation Model Concentration

The most striking feature of 2025's investment landscape is the concentration at the top:

**OpenAI** reached a $500 billion valuation—making it the most valuable private company in history.

**Anthropic** achieved a $183 billion valuation, positioning it as the clear second player in foundation models.

Together, these two companies represent nearly 10% of all unicorn value globally. Foundation model companies raised $80 billion in 2025—40% of total AI funding.

---

> **Key Insight**: This isn't speculative investment. These valuations are backed by explosive revenue growth. OpenAI's annualized revenue reached $12.7 billion with 800 million weekly active users. The fundamentals are real.

---

## What This Means

The AI investment supercycle signals that major institutional investors have reached consensus: AI represents a generational technological shift comparable to the internet itself. Capital is flowing accordingly.

For enterprises, this means:

1. **Innovation velocity will accelerate** — Well-funded AI companies will ship improvements rapidly

2. **Consolidation is coming** — Expect M&A activity as leaders acquire capabilities

3. **Talent competition intensifies** — AI talent remains the scarcest resource

4. **Infrastructure demands grow** — Data centers, chips, and energy become strategic assets

# Enterprise AI Transformation

*From experimentation to production-scale deployment*

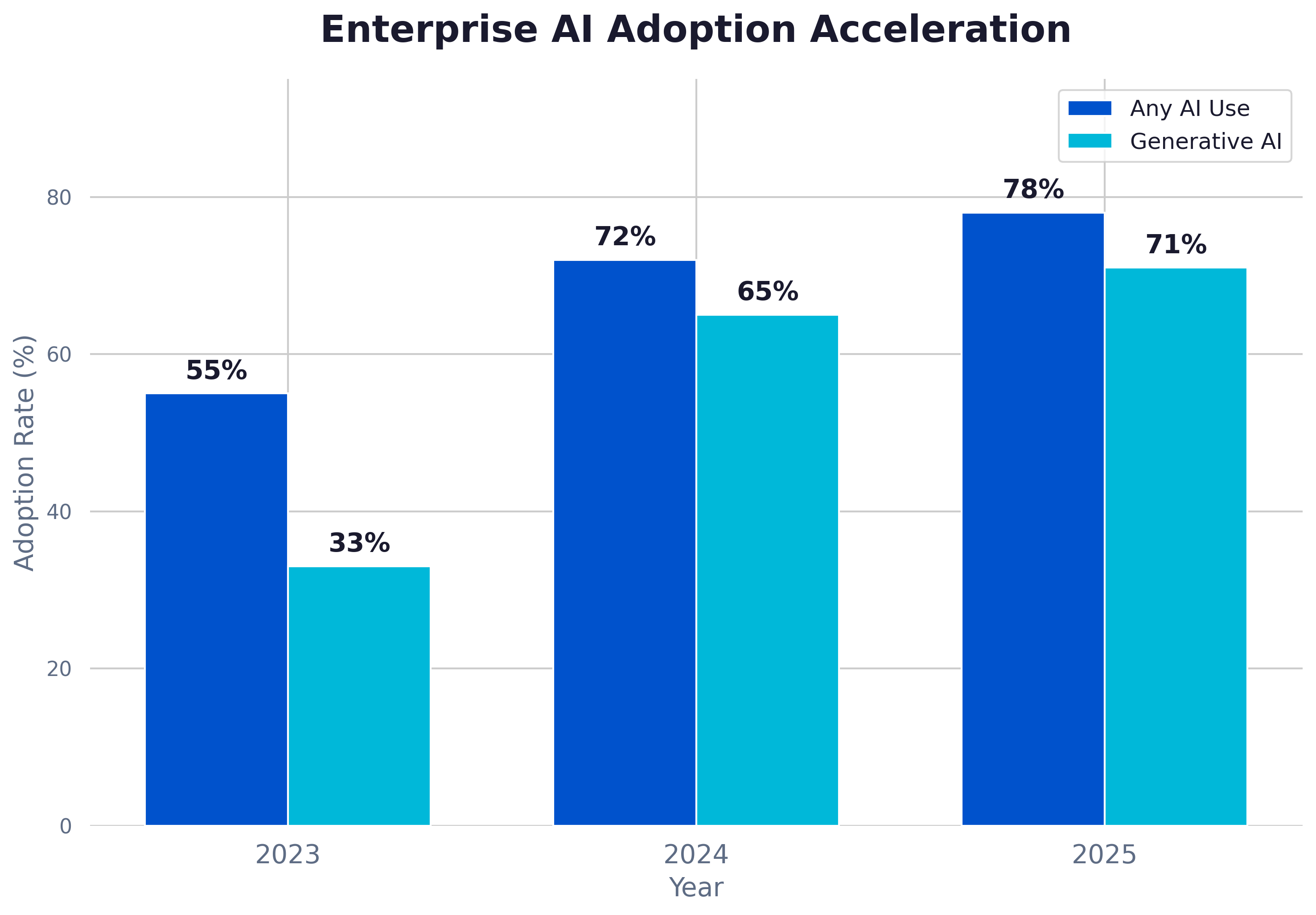

## The Adoption Acceleration

Enterprise AI has crossed the chasm. What was experimental in 2023 is now operational in 2025.

| Year | Any AI Use | Generative AI |

|------|----------:|--------------:|

| 2023 | 55% | 33% |

| 2024 | 72% | 65% |

| 2025 | 78% | 71% |

The jump from 55% to 78% in just two years represents the fastest enterprise technology adoption in modern history—faster than cloud computing, mobile, or even the internet.

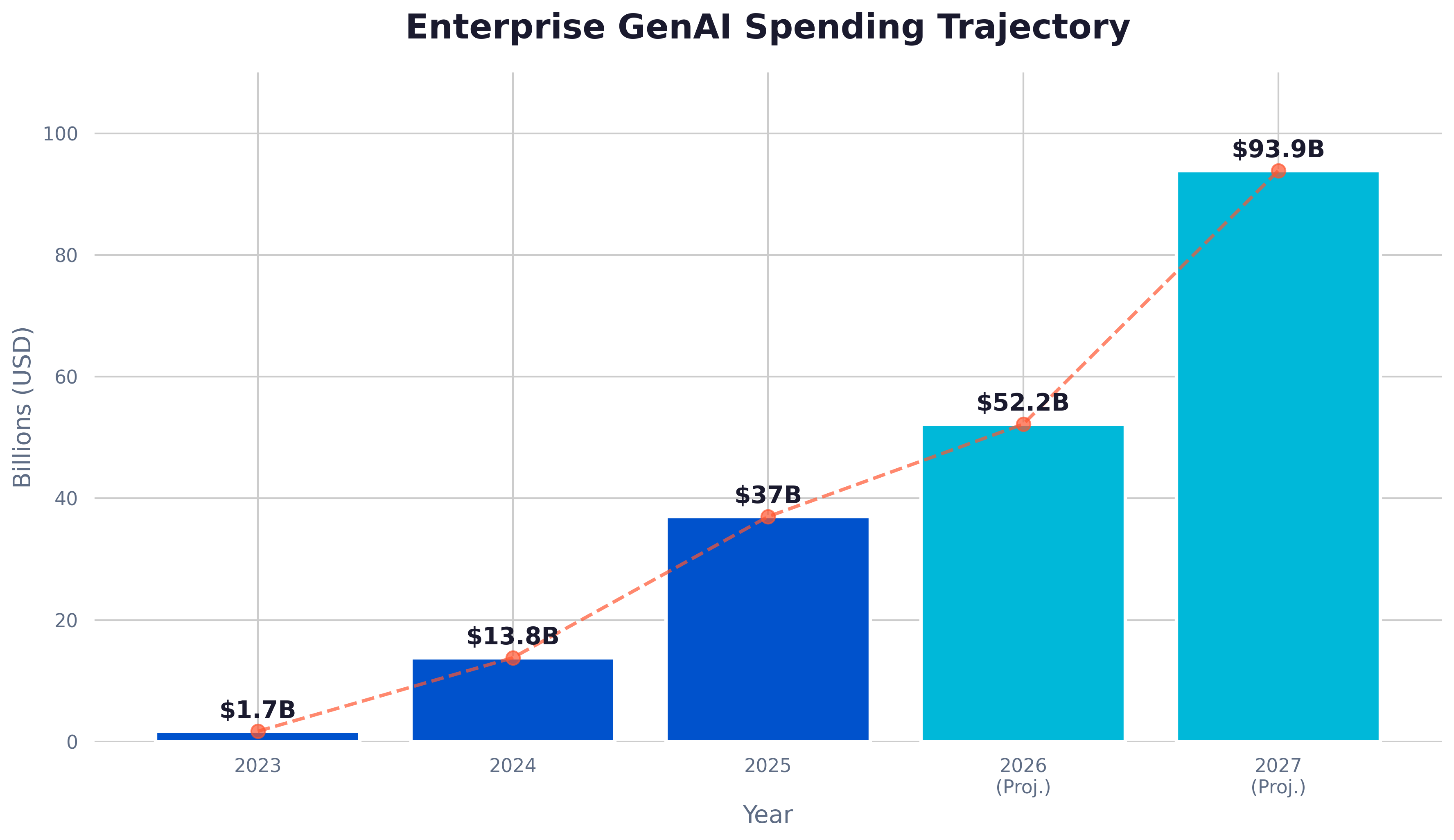

## Spending Trajectory

Enterprise GenAI spending tells an even more dramatic story:

| Year | Spending |

|------------------|----------|

| 2023 | $1.7B |

| 2024 | $13.8B |

| 2025 | $37B |

| 2026 (Projected) | $52.2B |

| 2027 (Projected) | $93.9B |

From $1.7 billion to $37 billion in two years—a 21x increase. Projections suggest this will reach nearly $100 billion by 2027.

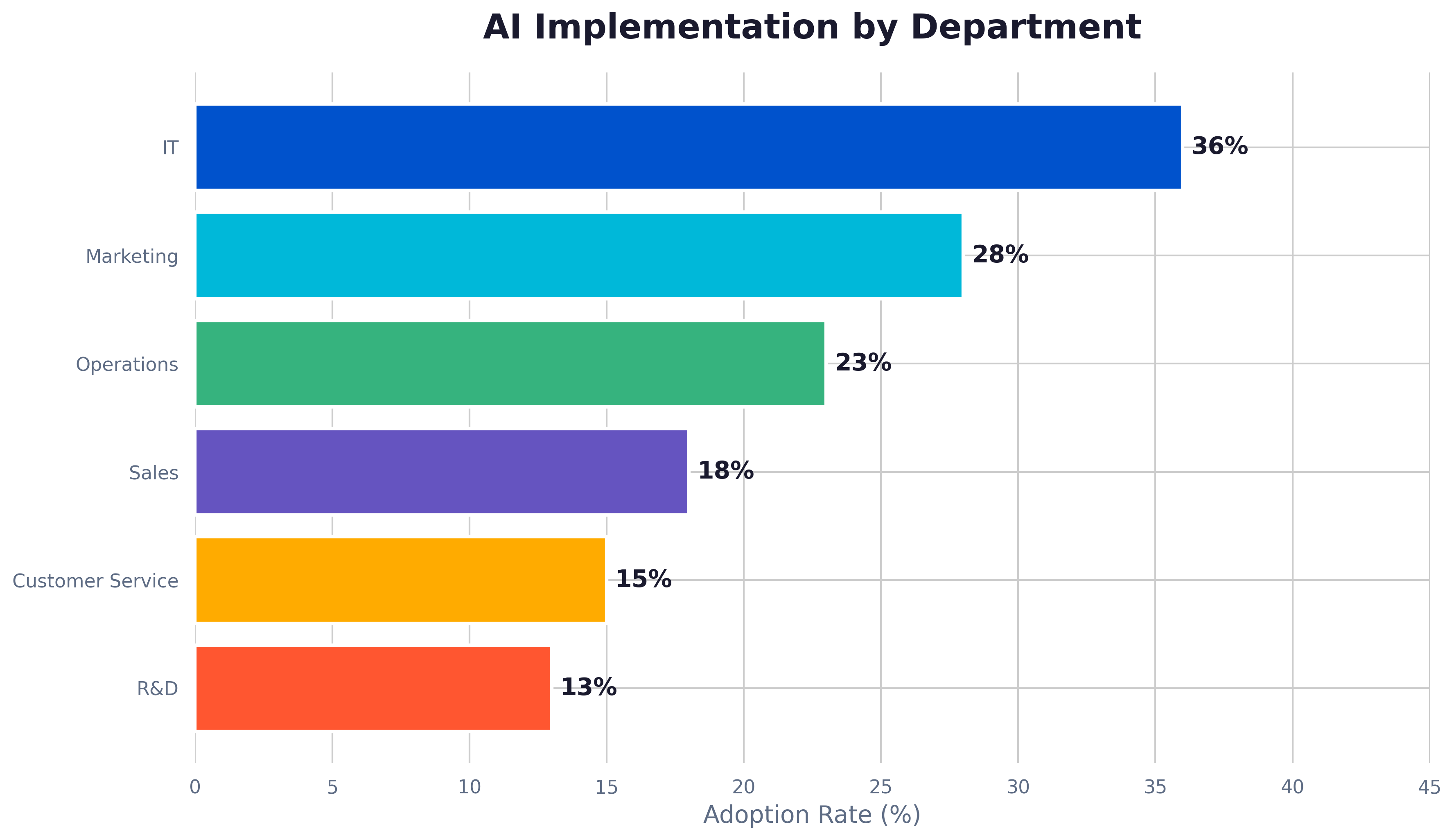

## AI Implementation by Department

AI adoption varies significantly across organizational functions:

| Department | Adoption Rate |

|------------------|--------------|

| IT | 36% |

| Marketing | 28% |

| Operations | 23% |

| Sales | 18% |

| Customer Service | 15% |

| R&D | 13% |

IT leads adoption—unsurprisingly, as technical teams are best positioned to evaluate and deploy AI tools. Marketing follows closely, driven by content generation and personalization use cases.

The opportunity: Sales, Customer Service, and R&D remain under-penetrated. These departments represent significant automation potential that many organizations haven't yet captured.

## The Buy vs. Build Shift

Perhaps the most significant strategic shift in 2025 is the reversal of the build vs. buy equation.

**2024**: 47% of enterprise AI solutions built internally

**2025**: Only 24% built internally—76% are now purchased

This dramatic flip reflects three realities:

1. **Commercial AI products have matured** — Off-the-shelf solutions now match or exceed internal capabilities

2. **Build costs have exploded** — Recruiting AI talent, managing infrastructure, and maintaining models is expensive

3. **Speed matters** — Purchasing gets you to production in weeks, not years

---

> **Key Insight**: The era of "we'll build our own AI" is largely over for most enterprises. The competitive advantage has shifted from building AI to *deploying and integrating AI effectively*.

---

## What Separates Leaders from Laggards

Research from McKinsey and Deloitte identifies clear patterns separating AI leaders:

**Leaders:**

- Deploy AI in production (not just pilots)

- Integrate AI into core workflows

- Measure ROI rigorously

- Invest in change management

- Have executive sponsorship

**Laggards:**

- Stuck in perpetual pilot mode

- AI remains siloed in IT

- No clear ROI metrics

- Underinvest in training

- Lack C-suite commitment

The gap is widening. Organizations that haven't operationalized AI by end of 2025 risk falling permanently behind.

# Emerging Technology Markets

*Growth trajectories reshaping the decade ahead*

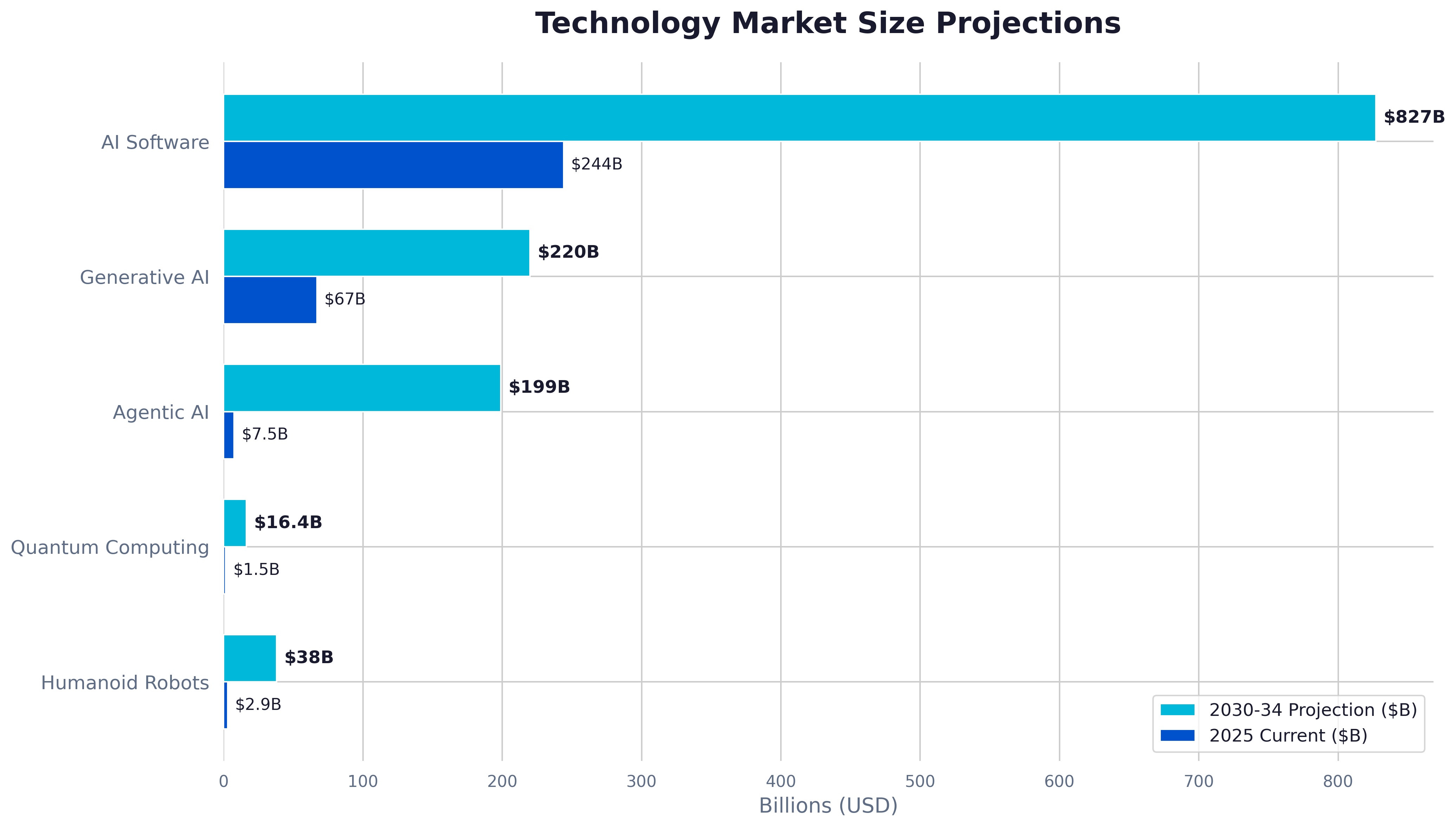

## Market Size Projections

Beyond current AI adoption, several technology markets are positioned for explosive growth through 2030-2034:

| Technology | 2025 Current | 2030-34 Projection | CAGR |

|-------------------|-------------:|-------------------:|------:|

| AI Software | $244B | $827B | 27.7% |

| Generative AI | $67B | $220B | 29.0% |

| Agentic AI | $7.5B | $199B | 43.8% |

| Quantum Computing | $1.5B | $16.4B | 30.9% |

| Humanoid Robots | $2.9B | $38B | 45.5% |

The numbers reveal where the next wave of transformation will come from.

## The Growth Leaders

### Humanoid Robots (45.5% CAGR)

The highest growth sector is perhaps the most surprising: humanoid robots.

Morgan Stanley projects this could become a $5 trillion market by 2050. Tesla's Optimus, Figure AI, and Boston Dynamics are racing to production. China has declared humanoid robotics a national priority.

The convergence of AI (for intelligence), improved batteries (for power), and advanced materials (for dexterity) has made humanoid robots commercially viable for the first time.

### Agentic AI (43.8% CAGR)

Agentic AI—autonomous systems that can plan, reason, and execute complex tasks—represents the next evolution of AI deployment.

Growing from $7.5B to $199B in under a decade, agentic AI will transform how enterprises automate workflows, manage operations, and serve customers.

### Quantum Computing (30.9% CAGR)

Quantum computing remains early-stage but is approaching commercial viability for specific use cases:

- Drug discovery

- Financial modeling

- Cryptography

- Materials science

- Optimization problems

First commercial quantum advantage is expected by 2027 in pharmaceutical research.

## What These Numbers Mean

These aren't independent trends—they're converging:

- **AI + Robotics** = Intelligent physical systems

- **AI + Quantum** = Breakthrough computational capabilities

- **Agentic AI + Everything** = Autonomous enterprise operations

Organizations planning for 2030 and beyond should track all three vectors.

---

> **Key Insight**: The 40%+ CAGR in humanoid robots and agentic AI suggests these technologies will move from "interesting experiments" to "operational necessity" within 5 years. Planning should start now.

# AI Capabilities Evolution

*Benchmark improvements and capability breakthroughs*

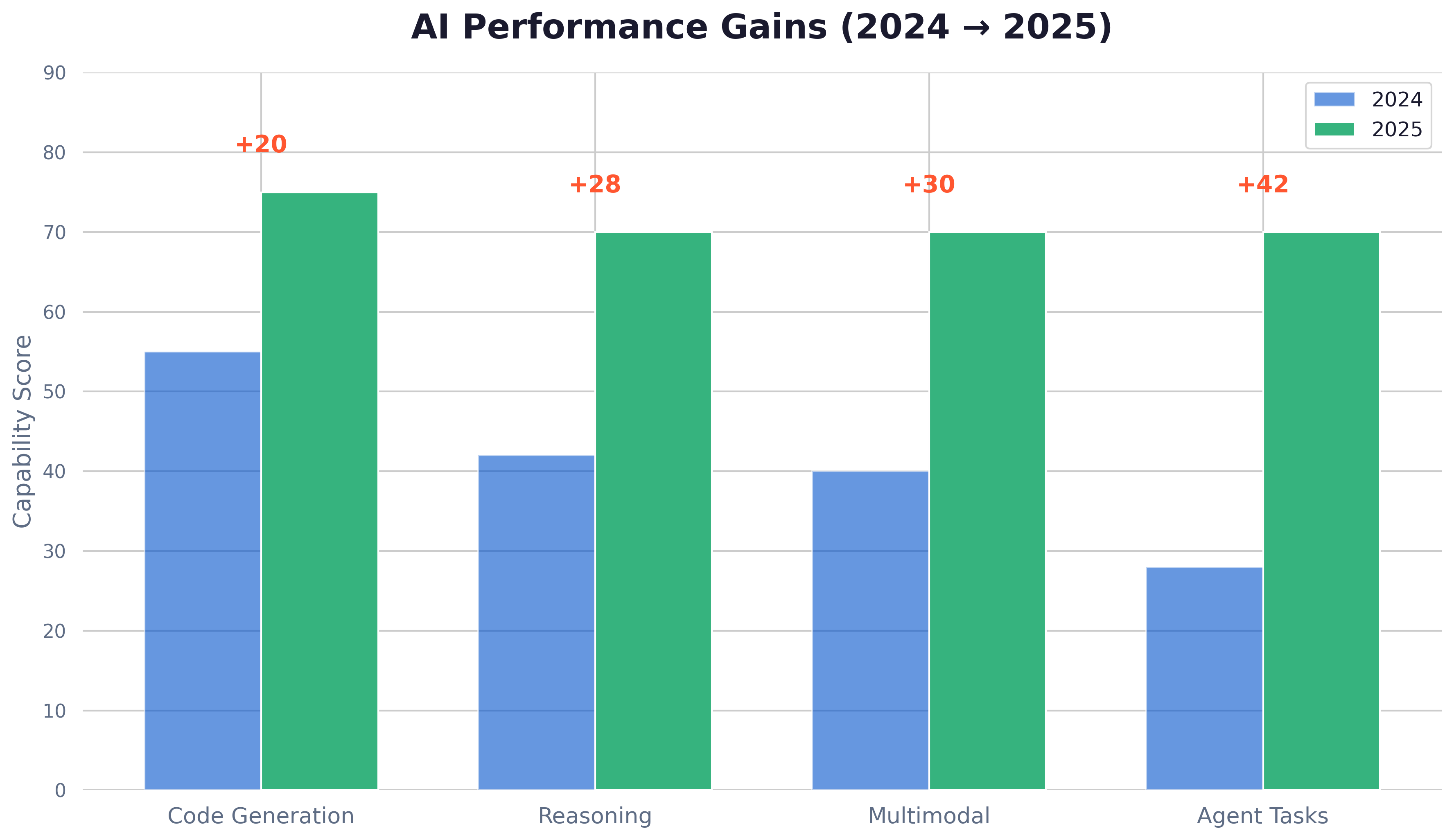

## Performance Gains (2024 → 2025)

AI capabilities improved dramatically across every major dimension in 2025:

| Capability | 2024 Score | 2025 Score | Improvement |

|-----------------|----------:|----------:|------------:|

| Code Generation | 55 | 75 | +20 points |

| Reasoning | 42 | 70 | +28 points |

| Multimodal | 40 | 70 | +30 points |

| Agent Tasks | 28 | 70 | +42 points |

The most dramatic improvement came in agent tasks—the ability of AI systems to autonomously plan and execute multi-step workflows. This capability essentially didn't exist at scale in 2024; by 2025, it's approaching production-ready.

## The Benchmark Saturation Problem

AI capabilities are advancing so rapidly that evaluation frameworks can't keep pace.

In 2024, researchers introduced several new benchmarks designed to challenge frontier AI models:

- **MMMU** (Multimodal understanding)

- **GPQA** (Graduate-level reasoning)

- **SWE-bench** (Software engineering)

Within one year, scores on these "hard" benchmarks rose dramatically:

| Benchmark | 2024 Score | 2025 Score | Improvement |

|-----------|----------:|----------:|-------------:|

| MMMU | 56.8% | 75.6% | +18.8 points |

| GPQA | 41.3% | 90.2% | +48.9 points |

| SWE-bench | 4.4% | 71.7% | +67.3 points |

Benchmarks designed to measure the frontier become saturated within months. This forces constant creation of harder evaluation frameworks—a good problem to have, but one that makes capability assessment challenging.

## Emerging Technology Maturity

Beyond pure AI, related technologies show varying levels of readiness:

| Technology | Maturity | Adoption | Impact Potential |

|------------|:--------:|:--------:|:----------------:|

| Generative AI | High | High | Very High |

| Agentic AI | Medium | High | Very High |

| Quantum Computing | Low | Very Low | High |

| Humanoid Robots | Low-Medium | Very Low | High |

| Brain-Computer Interface | Very Low | Minimal | High |

**Generative AI** is mature and widely adopted—the implementation phase is well underway.

**Agentic AI** has medium maturity but high adoption, suggesting enterprises are deploying despite remaining limitations.

**Quantum, Robotics, and BCI** remain early but carry transformative potential.

---

> **Key Insight**: The +42 point improvement in agent tasks is the headline number. It signals that AI is graduating from "assistant that responds" to "agent that acts." This shift will define 2026.

# The Rise of Agentic AI

*Autonomous systems transform from concept to enterprise reality*

## What is Agentic AI?

Agentic AI refers to AI systems that can:

- **Plan** — Break complex goals into steps

- **Reason** — Make decisions based on context

- **Execute** — Take actions autonomously

- **Learn** — Improve from feedback

- **Persist** — Maintain state across sessions

Unlike traditional AI assistants that respond to individual prompts, agentic systems can handle multi-step workflows with minimal human intervention.

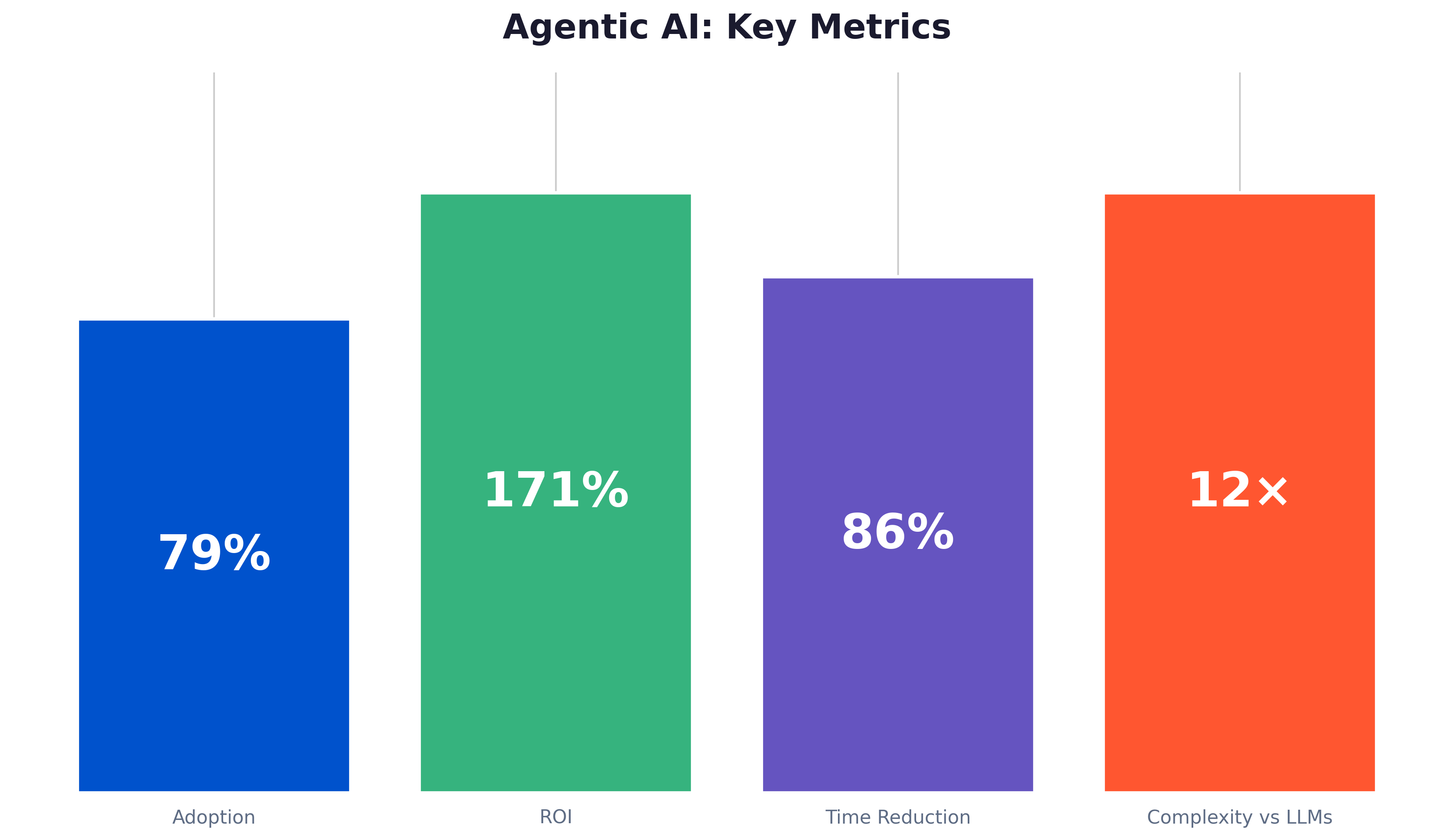

## The Numbers

Agentic AI adoption has been remarkably swift:

79%

Organizations with agentic AI adoption

171%

Average ROI reported

86%

Task time reduction

12×

More complex tasks vs traditional LLMs

These aren't pilot metrics—they're production results from organizations deploying agentic systems at scale.

## The Agent Workforce Revolution

Gartner's projection is stark:

> By 2028, 15% of day-to-day work decisions will be made autonomously by agentic AI—up from 0% in 2024.

We're witnessing the birth of a new category of digital worker. Not replacing humans, but augmenting them with autonomous capabilities that handle routine decisions and workflows.

## Current Adoption Patterns

- **45%** of Fortune 500 companies are piloting agentic systems

- **40%** of Fortune 100 firms use Microsoft's AutoGen framework

- Framework usage (AutoGen, LangGraph, CrewAI) is up **920% year-over-year**

## Key Use Cases

Agentic AI is finding traction in:

**Code Development**

- GitHub Copilot Workspace

- Cursor

- Devin (autonomous software engineer)

**Enterprise Workflows**

- Salesforce Einstein agents

- ServiceNow virtual agents

- SAP Joule agents

**Research & Analysis**

- Multi-step research tasks

- Document analysis and synthesis

- Competitive intelligence

**Customer Operations**

- Autonomous customer service

- Complex case resolution

- Proactive outreach

---

> **Key Insight**: The 79% adoption rate with 171% ROI suggests agentic AI has crossed from "interesting technology" to "competitive necessity." Organizations without an agentic AI strategy are falling behind.

# Strategic Outlook: 2026 and Beyond

*Critical trends shaping the next wave of innovation*

The data in this report points to six strategic predictions for 2026 and beyond:

---

## 1. Agentic AI Dominance

**60% of new enterprise AI deployments will include agentic capabilities by end of 2026.**

The shift from assistive to autonomous AI is accelerating. Organizations that master agentic deployment will gain significant operational advantages.

---

## 2. Model Commoditization

**Open-source models will reach parity with proprietary models for 80% of enterprise use cases.**

Llama, Mistral, and other open models are closing the capability gap. This will pressure pricing and shift competitive advantage from "having AI" to "deploying AI effectively."

---

## 3. AI Regulation Wave

**US federal AI legislation will pass, following EU AI Act implementation and 131 state-level laws.**

The regulatory environment is tightening globally. Compliance will become a strategic function, not just a legal one.

---

## 4. Quantum Advantage

**First commercial quantum computing advantage demonstrated in drug discovery by 2027.**

While still early, quantum computing will achieve its first meaningful commercial results within two years. Pharmaceutical and materials science companies should begin preparation.

---

## 5. Humanoid Scale-Up

**Humanoid robot shipments reach 115,000 units globally by 2027, led by China manufacturing.**

The humanoid robotics industry will scale from research to production. Manufacturing, logistics, and elder care are early adoption sectors.

---

## 6. AI Infrastructure Boom

**Hyperscaler AI capex exceeds $300B annually, driving massive data center buildout.**

Microsoft, Google, Amazon, and Meta's combined AI infrastructure investment will reshape energy markets, real estate, and chip manufacturing globally.

---

> **Key Insight**: These six trends are interconnected. Agentic AI requires infrastructure. Regulation shapes deployment. Commoditization accelerates adoption. Leaders will navigate all vectors simultaneously.

# Key Takeaways for Business Leaders

## Immediate Actions (2025)

### 1. Audit AI Readiness

Assess your current AI capabilities against the 78% adoption benchmark. If you're not deploying AI in production, you're behind the majority of enterprises.

Questions to ask:

- What AI tools are in production today?

- What's our AI spend relative to peers?

- Do we have executive sponsorship for AI initiatives?

### 2. Evaluate Agentic Pilots

With 79% adoption and 171% ROI, agentic AI demands attention. Identify three high-value workflows that could benefit from autonomous AI agents.

Starting points:

- Customer service escalation handling

- Data analysis and reporting

- Code review and documentation

### 3. Review Build vs. Buy

The 76% purchase rate suggests commercial solutions have matured. Reassess any internal AI development projects.

Ask:

- Can we buy this capability instead?

- What's the true cost of building internally?

- How much time would buying save?

### 4. Strengthen Data Infrastructure

AI success requires quality data foundations. Audit your data readiness:

- Data quality and cleanliness

- Access and governance

- Integration capabilities

---

## Strategic Planning (2026-2028)

### 1. Prepare for Regulation

EU AI Act compliance deadlines are approaching. US federal legislation is expected. Build compliance into your AI strategy now.

### 2. Develop AI Governance

233 AI incidents in 2024 (up 56.4%) highlight risk management needs. Establish:

- AI ethics guidelines

- Risk assessment frameworks

- Incident response procedures

### 3. Explore Emerging Tech

Quantum computing and humanoid robotics are approaching commercial viability. Assign someone to track developments and identify pilot opportunities.

### 4. Build Agent-Ready Architecture

Multi-agent systems will transform enterprise workflows. Ensure your technology stack can support:

- Agent orchestration

- Tool integration

- State management

- Monitoring and observability

---

## Investment Priorities

| Priority | Rationale |

|----------|-----------|

| **Generative AI Tools** | 71% enterprise adoption, proven productivity gains |

| **Agentic AI Platforms** | 43.8% CAGR, highest growth potential |

| **AI Security & Governance** | Incident rates up 56.4%, regulation imminent |

| **Data Infrastructure** | Foundation for all AI initiatives |

---

## The Bottom Line

The organizations that will lead in 2030 are making AI investments today. The data is clear:

- **$202B** flowing into AI annually

- **78%** of enterprises already deploying

- **171%** ROI from agentic AI

- **43.8% CAGR** in autonomous systems

The question isn't whether to invest in AI. It's how fast you can move.