The AI Investment Supercycle

Unprecedented capital concentration reshapes the technology landscape

Record-Breaking Investment

2025 marks an inflection point in technology investment history. Global AI investment reached $202.3 billion—more than double the $100 billion invested in 2024 and representing a 75% year-over-year increase.

To put this in perspective: AI now captures 49% of all global venture funding. Nearly half of every venture dollar flows into artificial intelligence.

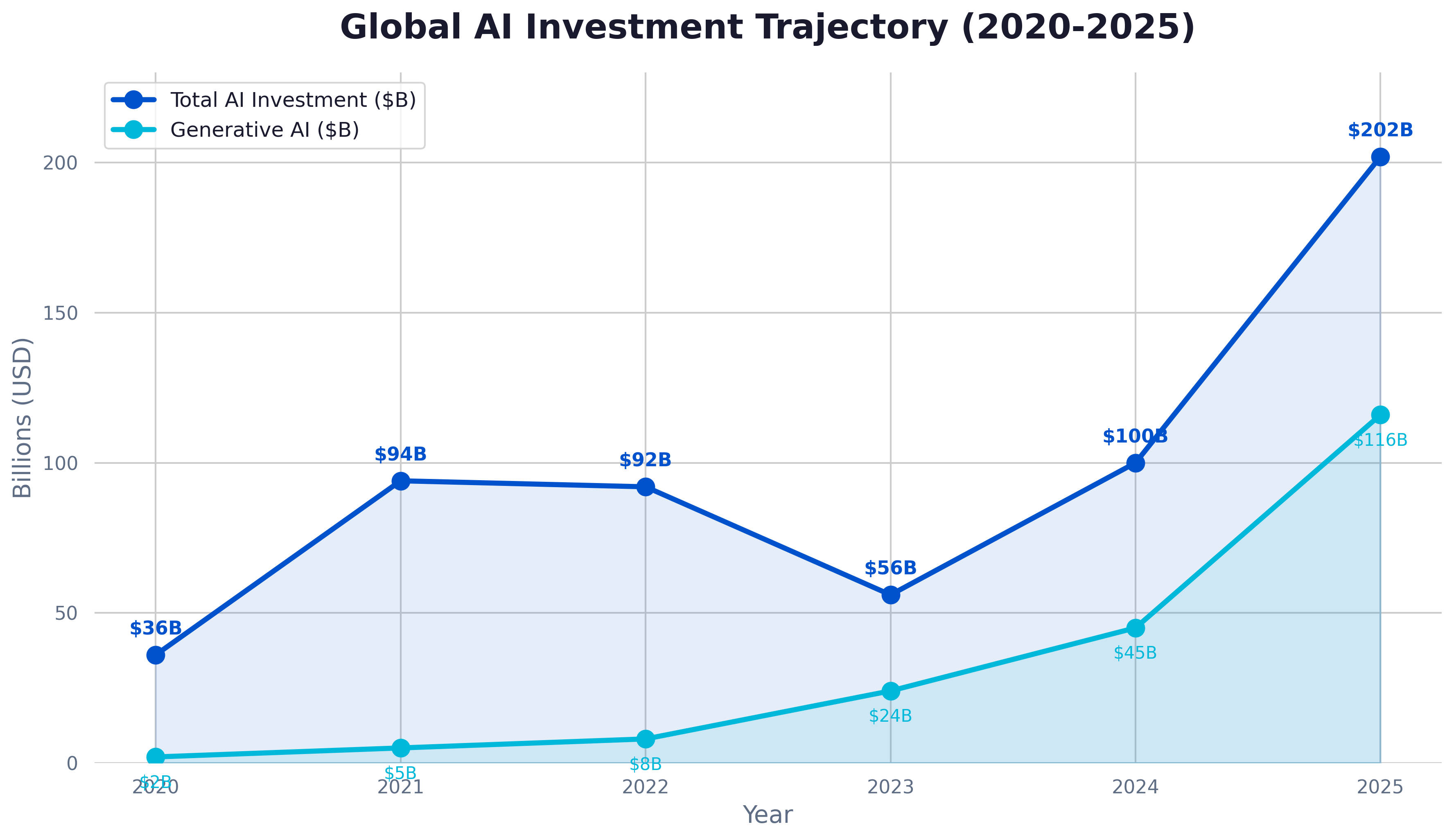

The Trajectory (2020-2025)

| Year | Total AI Investment | Generative AI |

|---|---|---|

| 2020 | $36B | $2B |

| 2021 | $94B | $5B |

| 2022 | $92B | $8B |

| 2023 | $56B | $24B |

| 2024 | $100B | $45B |

| 2025 | $202B | $116B |

The 2023 dip—often called the "AI winter scare"—proved to be a brief pause before explosive growth. Generative AI investment alone grew from $24B to $116B in just two years.

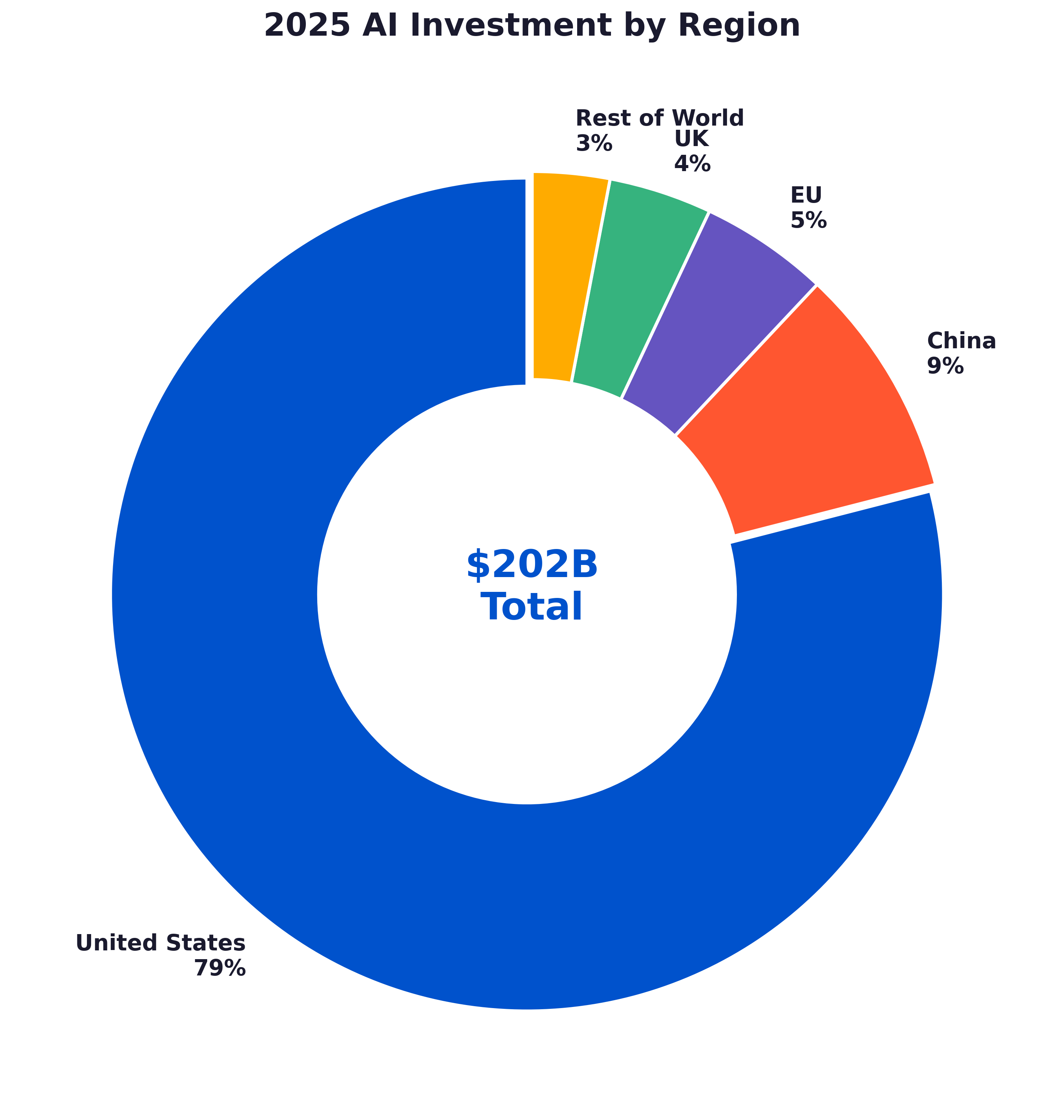

Regional Dominance

The United States has established overwhelming dominance in AI investment:

United States: 79% ($159B)

China: 9% ($18B)

European Union: 5% ($10B)

United Kingdom: 4% ($8B)

Rest of World: 3% ($6B)

US-based companies captured nearly 8 out of every 10 AI investment dollars globally.

The Foundation Model Concentration

The most striking feature of 2025's investment landscape is the concentration at the top:

OpenAI reached a $500 billion valuation—making it the most valuable private company in history.

Anthropic achieved a $183 billion valuation, positioning it as the clear second player in foundation models.

Together, these two companies represent nearly 10% of all unicorn value globally. Foundation model companies raised $80 billion in 2025—40% of total AI funding.

Key Insight: This isn't speculative investment. These valuations are backed by explosive revenue growth. OpenAI's annualized revenue reached $12.7 billion with 800 million weekly active users. The fundamentals are real.

What This Means

The AI investment supercycle signals that major institutional investors have reached consensus: AI represents a generational technological shift comparable to the internet itself. Capital is flowing accordingly.

For enterprises, this means:

Innovation velocity will accelerate — Well-funded AI companies will ship improvements rapidly

Consolidation is coming — Expect M&A activity as leaders acquire capabilities

Talent competition intensifies — AI talent remains the scarcest resource

Infrastructure demands grow — Data centers, chips, and energy become strategic assets